FNC News

Landowner News - A Tale of Two Hydrocarbons

For 18 months in a row, the average monthly price of West Texas Intermediate crude has bounced around between the range of $70-90. Global demand for oil continues to increase, with the IEA forecasting demand growth of 1.3 million barrels per day in 2024, a leg lower than OPEC’s more aggressive forecast of an increase of 2.25 million barrels per day this year. Matching increased demand is a continued increase in global production. All the while, OPEC plus has remained disciplined and continued to extend production cuts to keep prices in that $75-85 range, prices sufficient to fund sovereign budgets but not high enough to make the front page.

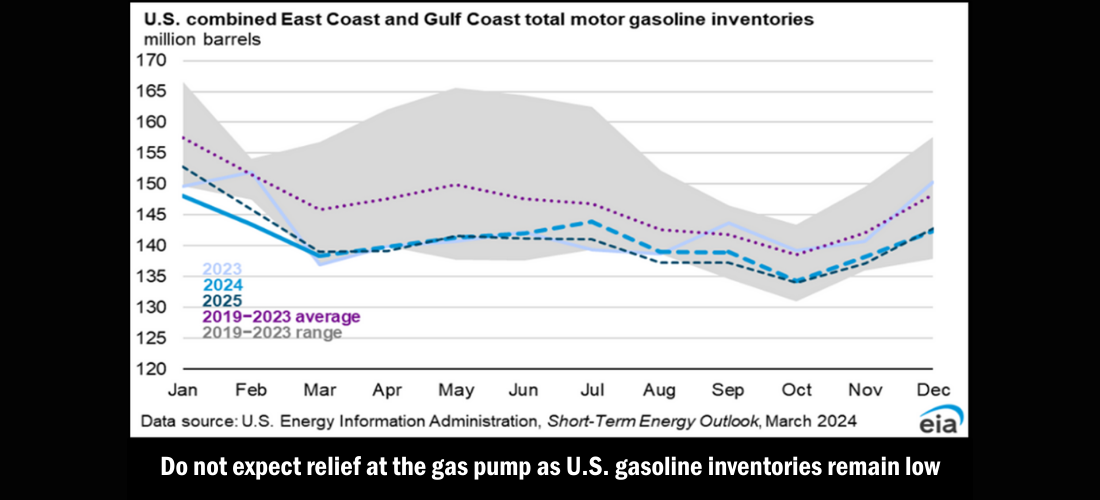

There is quiet strength in today’s domestic U.S. oil market. The oil production in the Permian Basin currently outpaces production of entire countries like Canada, Iraq, and Iran. In Europe, refineries have closed for planned or unplanned maintenance, resulting in US crude shipments into Europe hitting a new historical record in March. The U.S., however, has experienced its own bit of refinery outages resulting in lower gasoline inventories and increased prices at the pump (see table).

It is a vastly different tale when it comes to natural gas which, if one considers inflation, is at historically low prices. This miracle resource is caught in a perfect storm of mild weather, a surplus in gas storage, prolific gas wells, prolific ‘associated gas’ being produced from oil wells in the Permian basin, and bad news in the liquified natural gas (LNG) space ranging from the delay of the Golden Pass LNG terminal in Texas to the U.S. Administration announcing a temporary pause on pending LNG export decisions to non-Free Trade Agreement countries to assess, among other things, the impact of greenhouse gas emissions.

Domestic U.S. natural gas companies finally had their singular moment in the sun in 2022 with prices exceeding $8.00. While no one thought it would last, no one predicted just how far prices would and could fall. This industry is starting to feel like a small-market major league baseball team that must catch lightning in a bottle once every couple of decades just to make a magical championship run, with all other seasons being mired in perpetual disappointment and despair (okay, I’m a Kansas City Royals fan and I may be projecting).

Domestic U.S. natural gas companies of size and scale will fight to keep their capital development plans unchanged, especially those that are well hedged. Those without the necessary size and scale, however, will be forced to pull back on development and capital expenditures, which will affect their long-term growth and production trajectories and will have downstream effects on labor and equipment. Prices are so low that we may even see curtailment of existing production.

It truly is a tale of two hydrocarbons: the oil tale reading like a great summer novel and the natural gas tale reading like a Stephen King novel that never ends.

Interested in learning more, or have questions for our experts? Visit our website, www.fncenergy.com, and we’ll be happy to help.

More News

FNC Energy Industry Update | January 2026

Get the latest outlook on oil, gas, and what 2026’s energy roller coaster means for mineral owners.

Maximizing Your Land’s Potential with Renewable Energy

Farmers are exploring renewable energy leases to generate stable income while preserving farmland. Discover the benefits and considerations of wind and solar projects for landowners.

Farmers National Company Acquires Peoples Bank and Trust Farm Management Business

The acquisition adds more than 20,000 managed acres in Kansas and reflects a shared commitment to long‑term land stewardship.

U.S. Farmland Values Enter New Phase Shaped by Localized Market Signals

Regional differences underscore the need for local expertise as the agricultural land market adjusts.